Running a business in Louisiana is a rewarding, but challenging endeavor. Hurricanes, floods, severe storms, and litigation make Louisiana one of the riskiest states to do business in. Small businesses are especially hit hard. This is why having the right commercial coverage for your business is essential to safeguarding your investments and employees.

In this post, we’ll discuss why your business should have insurance, the unique factors contributing to high insurance premiums in Louisiana, types of coverages to consider, practical tips for reducing costs, and how to choose the right coverage. Let’s dive in!

Why Small Businesses in Louisiana Need Insurance

If you run any kind of business in Louisiana, it’s vital to have insurance. Having insurance helps protect your assets, covers the costs of lawsuits, supports recovery from natural disasters, and ensures you are compliant with state or industry regulations. For example, in Louisiana, all businesses with one or more employees are required to have workers’ compensation insurance with few exceptions. Additionally, commercial auto insurance is required for all company-owned vehicles.

For companies that have maritime workers, they may be subject to the Jones Act and the Longshore and Harbor Workers’ Compensation Act (LHWCA), which are both federal mandates protecting maritime workers.

Even if it’s not required by law to have coverage for your business, insurance helps protect you from financial ruin. Whether it's protecting your business from the next natural disaster or a cyberattack, commercial insurance will help your business recover and keep it running. This makes it worth the cost. But what makes insurance in Louisiana higher than other states? Let’s take a look.

Key Statistics on What Makes Insurance So Expensive in Louisiana

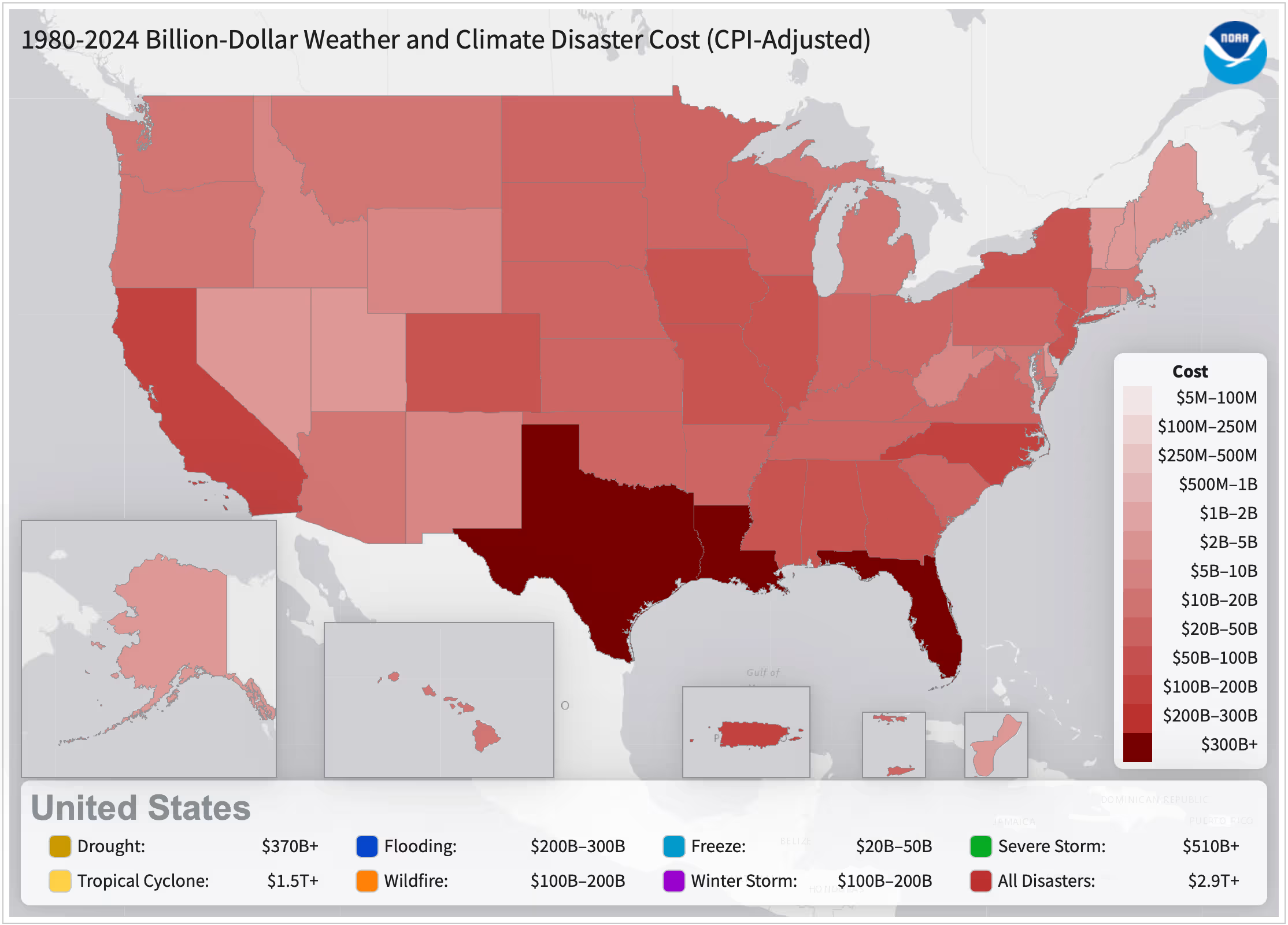

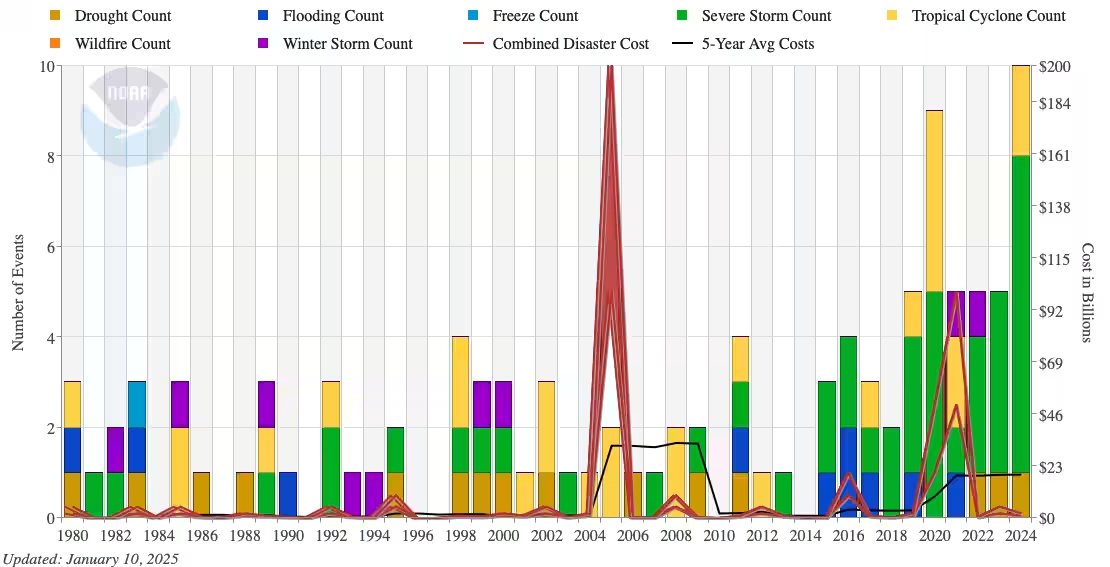

The biggest contributing factor to why insurance is expensive in Louisiana is due to the amount of major natural disasters Louisiana experiences. If we look at data from 1980-2024 provided by NOAA, it shows that there have been 403 confirmed weather disasters with losses exceeding $1 billion (CPI-adjusted) in the United States. That makes the annual rate 9 events per year; however, for the most recent 5 years, it is 23 events per year.

Looking at data just for Louisiana, the annual average from 1980–2024 is 2.4 events (CPI-adjusted); while the annual average for the most recent 5 years (2020–2024) is 6.8 events (CPI-adjusted). That means Louisiana has been involved in 27% of major natural disasters since 1980 and 30% since 2020.

The following chart shows the type of billion-dollar loss natural disasters that have affected Louisiana since 1980 and the costs associated with it. Predictably, flooding, severe storms, and tropical cyclones have caused the most damage monetarily.

The other factors that have affected insurance rates in Louisiana are the frequent lawsuits and limited competition among insurers in Louisiana. We discussed this at length in our Why Insurance Rates Are Rising in Louisiana post.

Types of Small Business Insurance In Louisiana

Every business is unique, which means your coverage needs are unique. Below is a list of the most common insurance coverage types businesses in Louisiana typically need to consider, but it’s best to check with your insurance broker to determine the exact coverages you need.

Practical Tips for Managing and Reducing Insurance Costs

With insurance costs continuing to rise across the country, there are some practical steps you can take to lower your insurance premiums.

- Bundling Policies: Bundling your insurance policies through one carrier can save you up to 20% off your premium.

- Install Safety Features: Installing security systems, cameras, sprinkler systems, water and gas leak detectors, and more can all help save your business money on insurance. For example, starting in 2026, commercial trucking companies in Louisiana will receive a 5% discount on insurance premiums when they install dashboard cameras on their trucks.

- Risk Management: Actively reducing risk by doing things like renovating old electrical or plumbing systems or replacing an older roof can reduce your premium amount.

- Policy Alignment: Tailor your policy to the actual cost to rebuild a company building rather than including the land’s value — this can significantly reduce the premium amount for commercial property insurance. Conversely, for assets like equipment, you’ll want to make sure you factor in the full replacement cost for new equipment since this will be more expensive compared to the value of your current used equipment.

Beyond these practical steps, legislative reform is what’s needed most to improve insurance costs in Louisiana. The 2026 session (March 9 - June 1) promises to build on 2025 tort reforms. In the coming weeks, we’ll be posting an article about Louisiana insurance issues that need to be addressed in the 2026 session.

How to Choose and Get the Right Commercial Insurance

Choosing the right insurance for your business increases in difficulty as your company grows in size and complexity. This is where having an independent insurance broker, like Lewis Mohr, can be an asset for your business. We are experts in risk management, helping determine not only the right coverages to protect your business but the appropriate policy limits to balance against losses and premium costs.

If you have questions about your current commercial policy or are interested in new policies for your business, please give us a call or send us a message. We have helped Louisiana businesses navigate the insurance market for more than 50 years and are ready to help find your business the right coverage.